If you have ever checked your credit score in one place and then had a lender pull a completely different number, you are not alone.

This is one of the most common questions people ask us, especially when they are preparing to buy a home, apply for a loan, or start working on their credit.

The truth is simple: you do not have just one credit score. You have many different credit scores, and they can vary depending on the scoring model, the bureau, the version being used, and the type of lender reviewing your credit.

If you want help understanding what is actually hurting your credit and what steps to take next, you can learn more about how The Dispute Coach works.

Important: Credit Karma, IdentityIQ, and similar monitoring tools can be very helpful for reviewing the information on your credit report. But the score you see there may not be the same score a mortgage lender uses.

You Have More Than One Credit Score

Most people think they have one credit score, but that is not how credit scoring works.

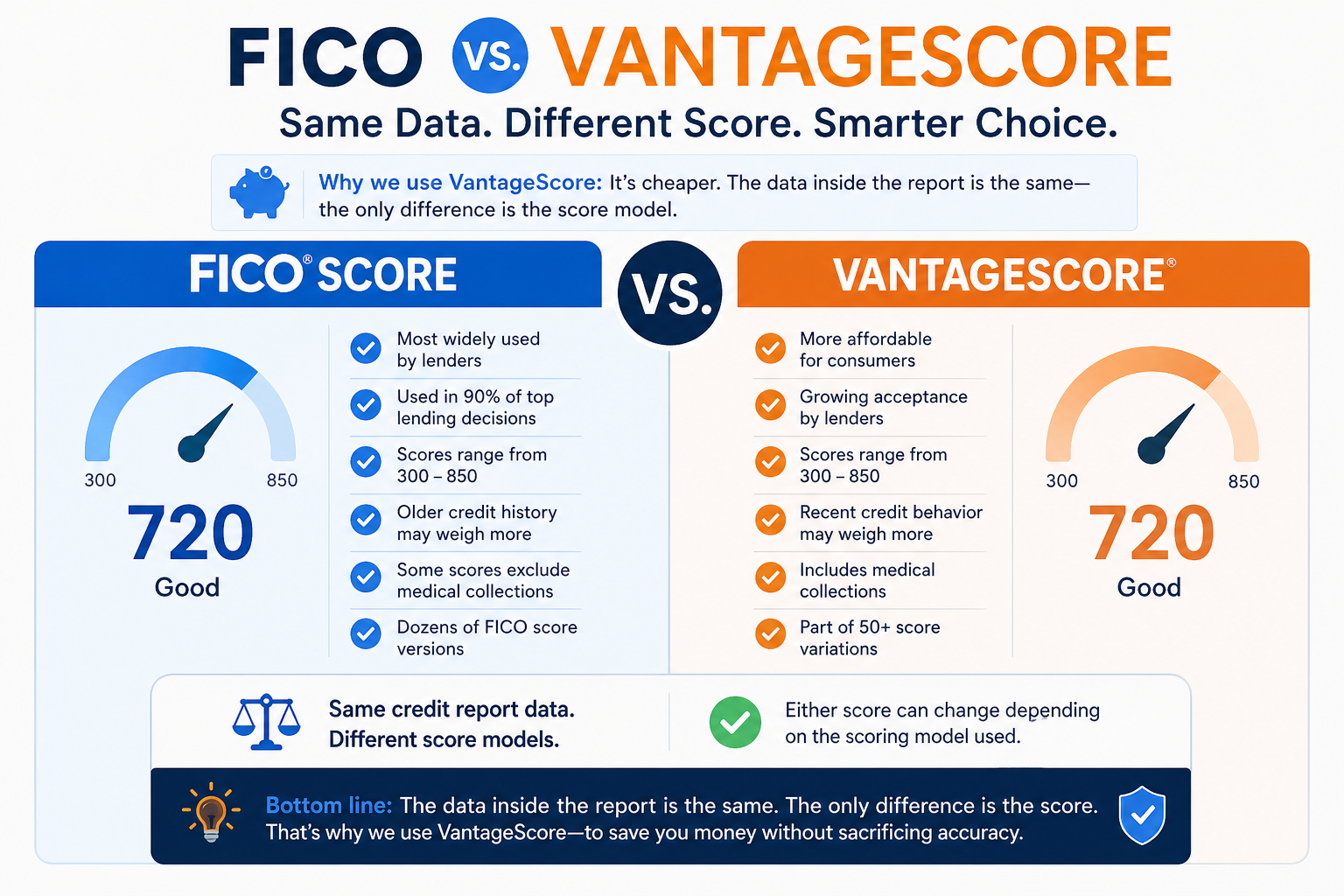

There are many different scoring models and versions. When you consider FICO, VantageScore, bureau-specific versions, mortgage scores, auto scores, bankcard scores, and updated model versions, there are well over 50 different score variations that may exist depending on the situation.

That means your score can be different depending on where you check it and what type of credit you are applying for.

Credit Karma and IdentityIQ Usually Show VantageScore

Credit Karma and IdentityIQ commonly show a version of VantageScore. VantageScore is a real credit scoring model, and it can be useful for monitoring your credit trends.

However, many lenders, especially mortgage lenders, do not use that same score when making approval decisions.

This is why someone may see a 720 on Credit Karma or IdentityIQ, but their mortgage lender may pull a 660 mortgage score. That does not automatically mean something is wrong. It usually means two different scoring models are being used.

Why We Use IdentityIQ

We use IdentityIQ because it gives clients access to the credit report data we need to help them review, organize, and challenge items on their credit reports.

The important thing to understand is this:

- the credit report data is what matters most for dispute work

- the accounts, balances, payment history, collections, inquiries, and personal information are pulled from the bureaus

- the score shown may be a VantageScore, not the same score a mortgage lender uses

- IdentityIQ is a more affordable way for clients to access and monitor their report data

In plain English, we are not using IdentityIQ because the score is the only score that matters. We use it because the report data gives us what we need to identify what may be helping or hurting your credit.

The score is helpful for tracking direction, but the report details are what guide the strategy.

What Is the Difference Between VantageScore and FICO?

VantageScore and FICO are both credit scoring models, but they do not calculate scores exactly the same way.

They may treat certain factors differently, including:

- credit card utilization

- recent late payments

- collections

- thin or limited credit history

- older accounts

- recent inquiries

- paid versus unpaid collection accounts

Because the formulas are different, the same credit report can produce two different scores.

Mortgage Lenders Usually Use Mortgage FICO Scores

When you apply for a mortgage, the lender usually pulls mortgage-specific FICO scores. These are not the same scores you typically see on free credit apps.

Mortgage scoring models can be more conservative, especially when it comes to negative accounts, high credit card balances, and recent derogatory activity.

This is why mortgage preparation is different from casually watching a credit app. If you are preparing to buy a home, you need to understand that your mortgage score may be lower than the score you are used to seeing.

You may also want to read what credit score you need to buy a house in 2026.

Why Your Scores May Not Match between all 3 bureaus

Your scores can vary betewen bureaus for several reasons.

1. Different bureaus

Experian, Equifax, and TransUnion may not all have the exact same information. If one bureau has a collection and another does not, the scores may differ.

2. Different reporting dates

Credit card balances and account updates do not always report on the same day. A balance that updated on one bureau may not have updated on another yet.

3. Creditors Report Different Places

A creditor does not have to report to all 3 bureaus. You may have an account that only chooses to report to 1 or 2 of the 3 bureaus.

Does That Mean Credit Karma or IdentityIQ Is Wrong?

No. It usually does not mean the tool is wrong.

It means the tool may be showing a different type of score than the lender uses.

Credit monitoring tools are still helpful because they allow you to review:

- new accounts

- collections

- late payments

- credit card balances

- inquiries

- personal information

- changes to your report over time

That information is extremely valuable, even if the score itself does not match your lender’s score.

Which Credit Score Should You Care About?

The score that matters most depends on your goal.

- Buying a home: your mortgage FICO scores matter most.

- Tracking progress: VantageScore can help you monitor trends.

- Repairing credit: VantageScore is a more inexpensive way to track the data.

- Applying for a credit card: the lender may use a bankcard or general FICO version.

- Buying a car: the lender may use an auto-specific score.

This is why we tell clients not to obsess over one number from one app. Instead, focus on improving the credit report itself.

What Actually Helps All Credit Scores?

Even though scoring models vary, most credit scores respond to the same core habits:

- making payments on time

- keeping credit card balances low

- avoiding unnecessary new accounts

- keeping positive accounts open when possible

- challenging inaccurate negative information

- building a stronger mix of positive accounts over time

If your score recently changed and you are not sure why, read why your credit score dropped and what to do about it.

Final Thoughts

Your credit scores can be different everywhere because not every company is using the same scoring model.

Credit Karma and IdentityIQ can be useful tools for monitoring your credit report and tracking general movement. But if you are applying for a mortgage, the score your lender pulls may be very different.

The best strategy is to stop chasing one app score and start focusing on the actual information inside your credit report. That is where the real work happens.

Want help understanding what is really hurting your credit? The Dispute Coach helps you review your report, organize your next steps, and take action with confidence.